Aligning Asset Acquisition With Income Spikes, Liquidity Events, and Business Cycles

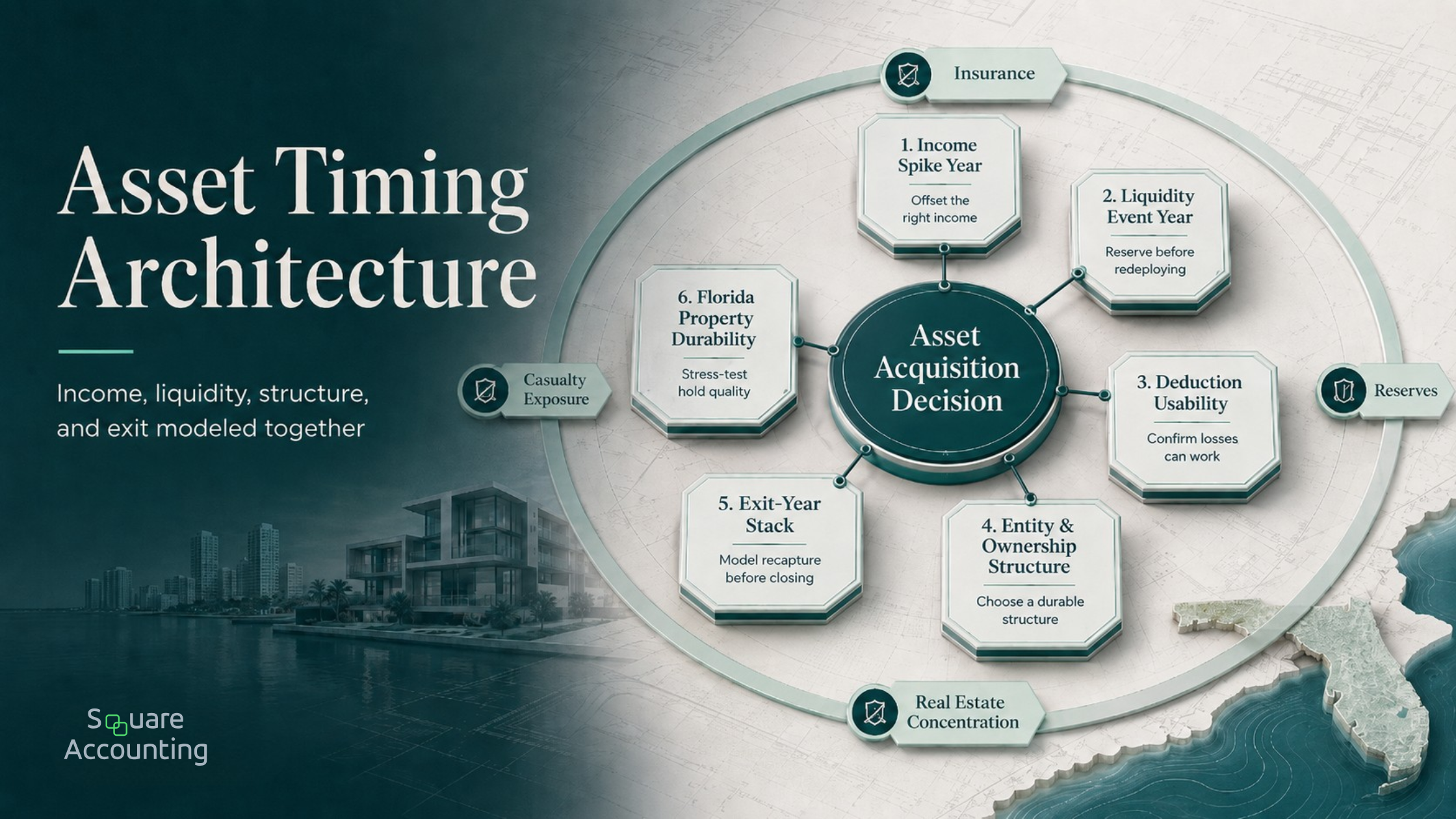

The strongest acquisition decisions are modeled as a system, with tax capacity, liquidity, structure, Florida property economics, and exit timing considered together.

Asset acquisition should be timed around tax capacity, not tax anxiety.

For a high-income Florida taxpayer, the immediate planning question is this:

Should we acquire the asset now, wait, finance it differently, or avoid it because the tax benefit will not survive the full multi-year sequence?

A year-end purchase may create a deduction. A better-planned acquisition creates usable tax value in the right year, preserves liquidity, supports the investment thesis, and does not create avoidable pressure in the exit year.

Use this first-screen framework before committing capital.

| Planning Trigger | Immediate Decision | Where Weaker Planning Breaks | Stronger Planning Response |

|---|---|---|---|

| Large W-2 Income, K-1 Income, Bonus Income, or Business Profit | Should deductions be accelerated into this year? | The deduction exists but cannot offset the intended income. | Confirm activity classification, placed-in-service timing, basis, at-risk exposure, passive loss limits, and projected income by bucket. |

| Business Sale, Equity Sale, Real Estate Sale, or Other Liquidity Event | Should new assets be acquired before or after the event? | The taxpayer redeploys capital quickly without modeling capital gain, NIIT, estimated tax payments, recapture, and reserves. | Build a liquidity-event tax stack before choosing acquisition timing or financing. |

| Real Estate Acquisition | Should depreciation be front-loaded? | Cost segregation or bonus depreciation creates suspended losses or future exit pressure. | Model current deduction usability against likely hold period, refinance plans, and disposition strategy. |

| Business Expansion | Should the tax benefit justify capital spending? | The purchase reduces tax but weakens operating liquidity. | Test debt service, working capital, hiring plans, insurance, replacement cycles, and tax payments together. |

| Florida Real Estate Concentration | Should the taxpayer hold, sell, exchange, or diversify? | No state personal income tax causes the federal tax stack and property-level economics to be underestimated. | Coordinate federal planning with homestead and non-homestead property tax economics, insurance, casualty exposure, reserves, and exit timing. |

The goal is not to buy assets because income is high. The goal is to align the acquisition with the years when deductions can be used, cash can be preserved, and exit consequences can be controlled.

Use our acquisition timing framework to test whether a purchase fits your income calendar, liquidity needs, and exit plan.

Why this matters in multi-year planning

High-income taxpayers often encounter asset acquisition at the same time income becomes unusually high. A founder is approaching a sale. A business owner has a record year. A physician or attorney receives a large bonus. A real estate investor exits one property and wants to redeploy capital. A family with concentrated stock wants to diversify into income-producing assets.

Those are planning windows, but they are not automatic buying signals.

A purchase made to solve this year’s tax problem can create next year’s liquidity problem, a passive loss problem that lasts longer than expected, or a recapture issue when the asset is sold. That is especially true for depreciation-heavy real estate planning, equipment purchases, short-term rental strategies, and acquisitions made soon before or after a business liquidity event.

Florida taxpayers have a specific version of this challenge. Florida’s lack of a state personal income tax often makes federal income tax planning the main battlefield. Florida law reflects that no income tax is levied on natural persons who are Florida residents and citizens.

That can be favorable, but it can also create a false sense of simplicity. Federal ordinary income, capital gain, NIIT, passive loss rules, depreciation, recapture, entity structure, and estate timing still need to be coordinated. Florida’s real estate economics also matter because property taxes, insurance, casualty risk, and reserve requirements can influence whether a tax-efficient acquisition remains financially durable.

Key takeaways

Asset acquisition timing should be based on deduction usability, not deduction availability.

An income spike creates tax capacity, but the deduction must land in the right activity and income bucket.

Liquidity-event years often create stacked exposure: capital gain, NIIT, estimated tax obligations, reinvestment pressure, and possible depreciation-related gain on real estate exits.

Depreciation-heavy planning can work well early and still create an avoidable problem later if hold period, exit strategy, and liquidity reserves are not modeled.

Entity and ownership structure should preserve options for financing, refinancing, gifting, sale, exchange, and estate planning.

For Florida taxpayers, no state personal income tax does not remove complexity; it shifts more attention to federal timing and property-level durability.

Aligning asset acquisition with income spikes, liquidity events, and business cycles

Aligning asset acquisition with income spikes, liquidity events, and business cycles means placing capital, deductions, debt, gain, and liquidity in the most efficient sequence.

The practical sequence is:

Identify the type and timing of income.

Determine whether a new asset can produce usable deductions.

Test the acquisition against liquidity and business-cycle risk.

Model the exit before closing.

Decide whether to accelerate, delay, finance, restructure, or pass.

This is a different exercise from asking whether an asset qualifies for depreciation or expensing. Qualification is the starting point. The planning value comes from whether the deduction improves the taxpayer’s position across several years.

1. What kind of income are you trying to offset?

The first question is not “What can we deduct?” It is “What income are we trying to offset, and can this deduction reach it?”

A taxpayer may have:

W-2 compensation

active business income

guaranteed payments or partnership income

portfolio income

passive rental income

capital gains from securities

capital gains from real estate

gain from the sale of a business

earnout or installment income

rollover equity or future transaction proceeds

The tax character matters because losses and deductions do not always move freely across these categories. Rental losses may be passive. Capital gains may not be reduced by ordinary deductions in the way the taxpayer assumes. Business deductions may be limited by basis, at-risk rules, or entity-level mechanics. Investment income may create NIIT exposure even when ordinary income planning has been addressed.

This is where sophisticated taxpayers still get surprised. The deduction is real, but the expected offset is not.

2. Will the deduction be usable in the year you need it?

A deduction is most valuable when it offsets income that would otherwise be taxed at a high marginal rate and when it does not create a worse future-year result.

A deduction can lose strategic value when it:

becomes a suspended passive loss

falls into a year that already has enough deductions

offsets lower-rate income while higher-rate income remains exposed

creates a net operating loss that does not align with the taxpayer’s expected income cycle

reduces future depreciation shelter in years when cash flow will still be taxable

accelerates basis reduction without a clear exit plan

This is why a single-year projection is not enough. We want to see the year before acquisition, the acquisition year, at least two forward years, and the likely exit year.

3. Does the acquisition strengthen or weaken liquidity?

Tax savings are not the same as liquidity.

A taxpayer may reduce federal tax in the acquisition year and still weaken the overall plan if the purchase requires too much cash, increases leverage at the wrong point in the business cycle, or creates ongoing capital demands.

This is especially relevant for Florida real estate. A property with an attractive depreciation profile may also require higher insurance reserves, larger repair reserves, stronger vacancy assumptions, and more conservative debt coverage. A short-term rental may create tax opportunity but also require active operating discipline, documentation, furnishing costs, cleaning systems, platform risk management, and cash reserves for seasonality.

For business owners, the same principle applies to equipment, vehicles, technology, leasehold improvements, or expansion assets. The acquisition should be tested against payroll, working capital, debt covenants, vendor exposure, and owner distributions.

The tax benefit should improve a strong capital decision. It should not rescue a weak one.

4. What happens in the exit year?

The exit year is where shallow acquisition planning becomes visible.

For real estate, the exit model should account for adjusted basis, depreciation taken or allowed, suspended passive losses, debt payoff, potential installment sale treatment, possible exchange planning, and unrecaptured §1250 gain. The IRS states that unrecaptured section 1250 gain from selling section 1250 real property is taxed at a maximum 25% rate.

That rate does not make depreciation unattractive. It makes timing and liquidity more important.

For business assets, the exit may involve purchase price allocation, ordinary income recapture, buyer negotiations, working capital adjustments, and entity-level consequences.

For portfolio or liquidity-event proceeds, the exit question may be less about the asset being acquired and more about the source of cash being redeployed. A taxpayer who sells appreciated stock, a business interest, or real estate to fund a new acquisition may create taxable gain before the new asset produces usable tax benefit.

The exit year should not be an afterthought. It should influence acquisition timing, entity selection, financing, reserve policy, and documentation from the beginning.

The federal tax layers that should be modeled before acquisition

A high-income acquisition plan usually involves several federal rules at once. The planning error is treating each rule as a separate topic instead of modeling how the layers stack.

| Federal Layer | Why It Matters Before Acquisition |

|---|---|

| Bonus Depreciation | Current rules can allow a significant first-year deduction for certain qualified property, but eligibility, placed-in-service timing, property type, and elections still matter. |

| Section 179 | Section 179 can create immediate expensing for qualifying property, but it is subject to annual dollar limits, phaseouts, taxable income limits, and property-specific rules. |

| Passive Activity Rules | A deduction may be limited or suspended if the activity is passive or if at-risk rules apply first. |

| Basis and At-Risk Limits | Entity-level debt, guarantees, capital contributions, and ownership structure can affect how much loss is usable. |

| NIIT | The Net Investment Income Tax can apply to certain investment income, including capital gains and some rental income, above statutory income thresholds. |

| Depreciation Recapture and Unrecaptured §1250 Gain | Prior depreciation can change the tax character and rate profile of gain when an asset is sold. |

| Estimated Tax Planning | A liquidity event or investment-income spike can create underpayment risk if withholding and quarterly payments are not coordinated. |

| Entity Structure | The wrong structure can limit loss usability, complicate financing, reduce flexibility, or create inefficient exit mechanics. |

Current IRS guidance describes a 100% additional first-year depreciation deduction for certain qualified property acquired after Jan. 19, 2025. IRS Publication 946 explains that Section 179 remains subject to specific dollar limits and other limitations, and IRS guidance states that NIIT applies at 3.8% to certain net investment income above statutory threshold amounts.

For sophisticated taxpayers, the key question is not whether one of these rules applies. It is whether several of them collide in the same year.

A common example is a Florida real estate investor who acquires a property after a large liquidity event, accelerates depreciation through a cost segregation study, and later sells earlier than expected. The acquisition-year deduction, passive loss classification, NIIT exposure, and exit-year depreciation-related gain all belong in the same model.

Read more on NIIT, depreciation, entity structure, and Florida real estate planning before making a capital decision.

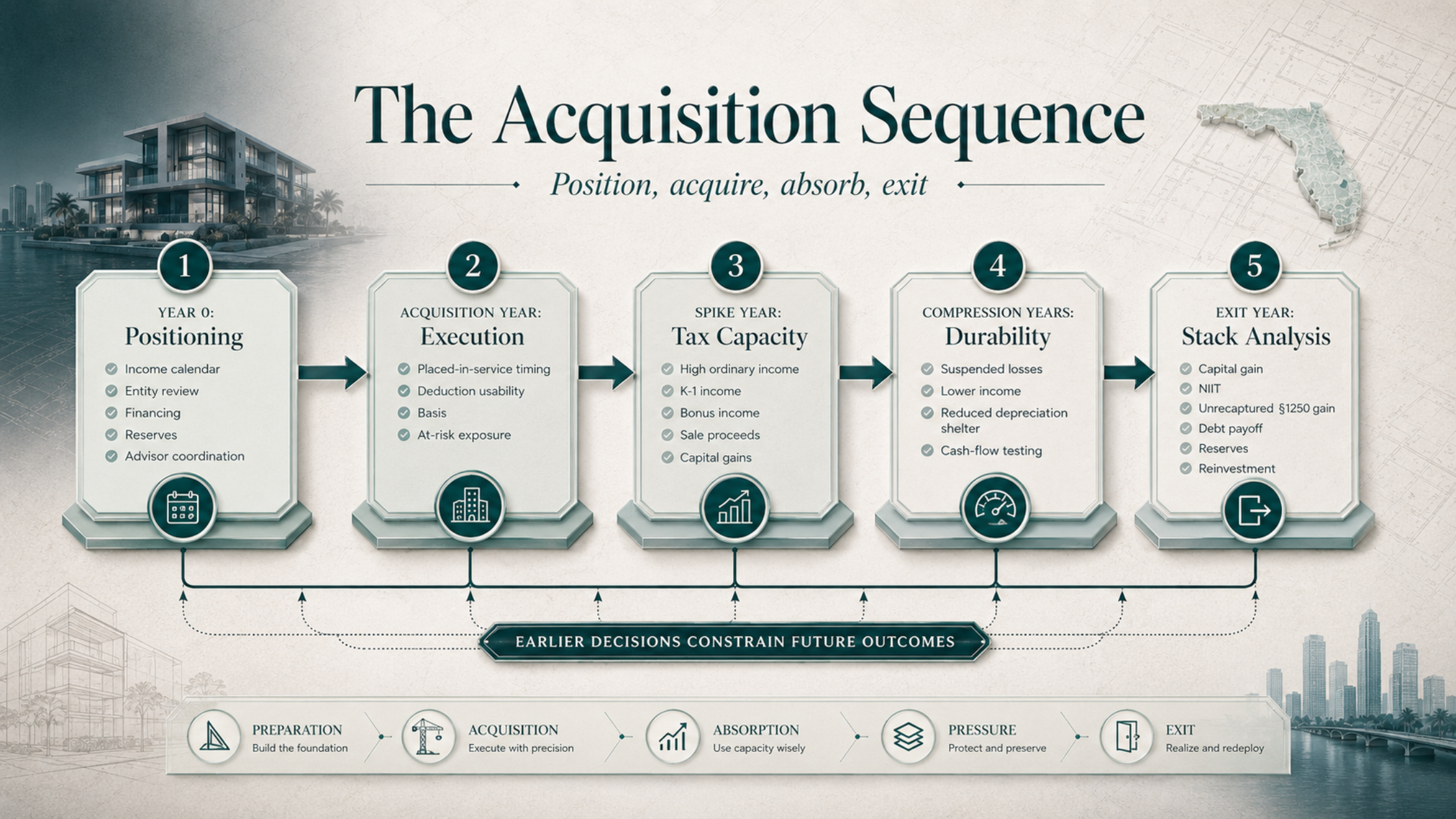

A better sequencing framework: acquisition year, spike year, compression years, exit year

The article’s central framework is a four-part sequence: the acquisition year, the spike year, the compression years, and the exit year. In practice, we also start with Year 0 because the most valuable decisions often happen before closing.

An acquisition should be tested through the full timeline: what it offsets now, what it leaves for later, and what it creates when the asset is sold.

Year 0: Pre-acquisition positioning

Before buying, the plan should define the taxpayer’s tax capacity and capital capacity.

Tax capacity asks:

What income is expected this year and over the next several years?

Is the income ordinary, capital, passive, active, portfolio, or mixed?

Which deductions already exist?

Which deductions are likely to be wasted, suspended, or deferred?

Will the taxpayer materially participate where participation matters?

Is the taxpayer trying to offset income that the asset cannot reach?

Capital capacity asks:

How much liquidity remains after closing?

What reserves are needed for tax, debt service, insurance, repairs, operating volatility, and family obligations?

How much debt is appropriate under a lower-income scenario?

What other planning opportunities compete for the same cash?

Would the asset still be attractive without the first-year tax benefit?

This is also the stage to assess advisor alignment. A CPA may focus on tax return mechanics. An attorney may focus on entity and liability protection. A lender may focus on debt service. An investment advisor may focus on asset allocation. The taxpayer needs one integrated view before capital is committed.

Acquisition year: Place the asset in service with the tax result in mind

For depreciation planning, the placed-in-service date matters. A contract, closing, or invoice does not always produce the intended tax result if the asset is not ready and available for its intended use.

The acquisition year should answer three questions:

What deduction is available?

What deduction is currently usable?

What deduction should be accelerated versus preserved?

The third question matters more now because a larger immediate deduction can look attractive but still be strategically inefficient. If the taxpayer already has enough deductions in the acquisition year, full acceleration may reduce future-year flexibility. If future income is expected to remain high, smoothing deductions may produce a better multi-year result. If the asset may be sold soon, the exit-year model may argue for restraint.

This does not mean acceleration is wrong. It means acceleration should be chosen, not assumed.

Spike year: Use tax capacity deliberately

A spike year may come from record business income, a large bonus, stock vesting, partnership income, a legal settlement, a business sale, or a real estate exit.

A spike year can be a strong acquisition window when:

the asset already fits the investment or operating plan

the deduction offsets the intended type of income

passive and at-risk limitations are addressed

the taxpayer has enough liquidity after closing

debt terms remain durable under lower-income projections

the hold period supports the depreciation and exit model

the entity structure preserves future options

A spike year can be a poor acquisition window when:

the purchase is being made mainly to reduce tax

the resulting losses are likely to be suspended

the transaction absorbs liquidity needed for tax payments

the taxpayer is also facing a major estimated tax obligation

the asset will require large reserves in the following year

the acquisition crowds out stronger planning tools

the exit is likely to occur before the tax timing benefit matures

The planning decision is not “high income means buy.” It is “high income creates capacity; what is the best use of that capacity?”

Sometimes that answer is an asset acquisition. Sometimes it is retirement plan design, charitable planning, sale-structure planning, installment planning, entity restructuring, gain harvesting, loss harvesting, or waiting.

Compression years: Avoid creating stranded deductions

Compression years are the years after the spike.

A business owner may sell a company and move from operating income to investment income. A professional may have an unusually high bonus year followed by normal income. A real estate investor may exit an appreciated property and then redeploy into assets with different cash-flow profiles. A taxpayer may accelerate several years of deductions into one year and then face taxable cash flow later with less depreciation shelter.

Compression years create two risks.

First, the taxpayer may have lower taxable income when future deductions arrive, making those deductions less valuable.

Second, the taxpayer may have higher taxable cash flow because too much depreciation was pulled forward. That can happen when a real estate acquisition produces a large first-year deduction but less annual shelter later.

This is not necessarily a reason to avoid acceleration. A deduction used in a high-rate year can be highly valuable. But the taxpayer should understand whether the plan is intentionally front-loaded or accidentally depleted.

Compression years are also where suspended passive losses should be monitored. A suspended loss is not worthless, but it is not the same as a current tax reduction. Its value depends on future passive income, disposition planning, and the taxpayer’s broader income profile.

Exit year: Model the stack before the sale

The exit-year stack should be modeled before the acquisition closes.

For a real estate exit, the model may include:

sale price and adjusted basis

depreciation taken or allowed

selling costs

debt payoff

capital gain

unrecaptured §1250 gain

NIIT exposure

suspended passive loss release

possible §1031 exchange planning

installment sale feasibility

charitable planning before a binding sale

estate and basis planning if a long-term hold is realistic

cash available to pay federal tax after debt and transaction costs

A deduction-heavy acquisition should be measured against the exit year, when gain, debt payoff, depreciation-related tax, estimated taxes, and reserve needs may converge.

For a business exit, the stack may include:

stock sale versus asset sale treatment

ordinary income versus capital gain allocation

depreciation and amortization recapture

escrow and earnout timing

rollover equity

state sourcing for non-Florida activity

estate planning before value becomes fixed

estimated tax and withholding decisions

The exit model is not pessimistic. It is the only way to know whether the acquisition-year benefit is worth the future trade-off.

We can help organize the acquisition year, spike year, compression years, and exit year into one planning model.

The “works early, breaks later” pattern in real estate depreciation

Many real estate tax strategies work early because depreciation is front-loaded.

A cost segregation study may identify shorter-life property. Bonus depreciation may accelerate eligible components. A short-term rental strategy may create a non-passive loss if the activity is structured and documented properly. A real estate professional may be able to treat rental losses differently if the statutory and material participation requirements are met.

The failure mode is not that these strategies are weak. The failure mode is that they are often modeled only through the first return.

A strategy can work early and break later when:

the loss is passive and cannot offset the income the taxpayer expected

the taxpayer’s material participation is assumed rather than documented

personal use or mixed-use patterns undermine the intended treatment

the property is sold before the timing benefit has matured

depreciation reduces basis and increases future gain pressure

refinancing proceeds are spent without reserving for future tax

insurance, repairs, vacancies, or debt service absorb the cash-flow benefit

the entity structure makes a later sale, exchange, gift, or estate plan harder

The more successful the taxpayer, the more important this becomes. High-income taxpayers often have enough complexity already. They do not need a deduction that creates a second-order problem because the original model stopped too early.

A stronger approach is to underwrite the tax strategy the same way an investor underwrites the asset: base case, downside case, early-sale case, and exit case.

Coordinating asset acquisition with business cycles

Business cycles matter because tax capacity and cash capacity do not always move together.

A taxpayer may have high taxable income and weak cash flow. A taxpayer may have strong liquidity after a sale but no immediate need for new tax deductions. A taxpayer may have lower current income in a down cycle but an unusually attractive opportunity to acquire assets at better pricing.

The acquisition decision should respect both cycles.

Expansion cycle

During expansion, taxable income may be high and deductions may be usable. But expansion also consumes cash.

Before buying assets in an expansion cycle, the taxpayer should test:

payroll and hiring plans

working capital needs

customer concentration

vendor and inventory commitments

debt covenants

owner distributions

estimated tax obligations

replacement and maintenance cycles

A tax deduction does not protect the business from overextension. In some cases, leasing, staged purchasing, or financing may preserve more flexibility than an outright acquisition.

Liquidity cycle

After a liquidity event, taxpayers often want to redeploy capital quickly. That instinct is understandable. Cash can feel unproductive, and a new acquisition may seem like a way to replace income, diversify, or create deductions.

The risk is compression. The liquidity-event year may already include capital gain, NIIT, estimated tax payments, legal fees, transaction costs, portfolio repositioning, and family or estate planning decisions. Adding a major acquisition before the tax stack is modeled can make the year harder to manage.

A staged redeployment plan may be more effective than immediate deployment. That does not mean doing nothing. It means separating cash into tax reserve, operating reserve, near-term allocation, and long-term acquisition capital before deciding what should be bought and when.

Down cycle

A down cycle can create better acquisition pricing, but lower income may reduce the immediate tax value of deductions.

That is not necessarily a problem. Asset quality, basis, financing terms, and long-term return may matter more than first-year tax benefit. A lower-income acquisition year can still make sense if the asset strengthens the long-term portfolio or if future income will make later deductions valuable.

The mistake is rejecting a good acquisition because the current-year deduction is less valuable, or accepting a weak acquisition because the current-year deduction looks attractive.

Exit cycle

As a business owner or investor approaches a sale, acquisition timing becomes more sensitive.

Purchasing assets shortly before a business sale may affect working capital, valuation, purchase price allocation, buyer diligence, and post-closing obligations. Buying real estate shortly before selling another asset may help diversify, but it can also strain liquidity if the sale is delayed, financing changes, or tax payments arrive sooner than expected.

The exit cycle should produce a capital calendar. The calendar should show expected closing dates, tax payment dates, reserve requirements, reinvestment windows, and decision deadlines. Without that calendar, taxpayers often make correct individual decisions in the wrong order.

Florida-specific planning considerations

Florida planning should not be forced into every tax topic. It matters here because acquisition timing, liquidity events, and real estate holding periods are directly affected by Florida’s tax and property environment.

For Florida taxpayers, federal tax planning is most useful when it is tested against property tax economics, insurance, casualty exposure, reserves, and real estate concentration.

No state personal income tax makes federal planning more important

For Florida residents, the absence of a state personal income tax often shifts the primary income tax analysis to federal law. That makes federal timing more important, not less important. Ordinary income, capital gain, NIIT, depreciation, passive losses, entity structure, and estate-related basis planning carry more of the income tax planning burden.

For taxpayers who own property or businesses outside Florida, the analysis may still include other state tax exposure. Florida residency does not erase tax obligations connected to non-Florida activity or property.

Real estate concentration can magnify exit-year pressure

Many Florida taxpayers are heavily concentrated in real estate: primary residence, rental homes, short-term rentals, commercial property, development land, or out-of-state replacement property.

That concentration can create a timing problem when multiple exits cluster. A taxpayer may sell one property, refinance another, exchange into a third, and acquire a short-term rental in the same planning window. Each move may be reasonable by itself. Together, they may create gain, debt, basis, depreciation, NIIT, and liquidity pressure that should be modeled as one system.

This is also where advisor fragmentation can hurt. The real estate broker sees the sale opportunity. The lender sees borrowing capacity. The CPA sees the return. The attorney sees the entity. The taxpayer needs one integrated federal and property-level exit plan.

Homestead and non-homestead property tax economics affect hold/sell decisions

Florida’s Save Our Homes assessment limitation generally limits annual increases in assessed value for qualifying homestead property to the lower of 3% or the change in CPI.

Investment property, second homes, and commercial property operate under different assessment-cap rules and may face different reassessment consequences after transfer or ownership changes.

This affects acquisition and exit planning because a Florida primary residence with a valuable homestead position may have a very different hold/sell profile than a rental property or non-homestead property. A property that is attractive from an income tax perspective may be less attractive after property tax reset risk, insurance, and carrying costs are modeled.

The decision is not simply “sell or hold.” It is whether the after-tax, after-insurance, after-property-tax economics still justify the holding period.

Insurance, casualty, and reserve planning are tax planning issues too

In Florida, insurance and casualty exposure can change the durability of a tax strategy.

A depreciation benefit may be meaningful in the acquisition year, but it does not eliminate the need for reserves. If insurance premiums rise, a roof must be replaced, a storm creates repairs, or occupancy drops, the taxpayer needs liquidity that is not already committed elsewhere.

This is why reserve policy belongs inside tax planning. A plan that reduces tax but leaves the taxpayer under-reserved is not an efficient plan. It is a timing trade with hidden fragility.

For Florida real estate investors, we generally want acquisition models to include tax reserve, insurance reserve, casualty reserve, capital expenditure reserve, and debt-service reserve. Those reserves may reduce the amount available for immediate acquisition, but they increase the likelihood that the strategy can survive the holding period.

Work with our team to coordinate asset acquisition timing with income spikes, liquidity events, and Florida-specific holding risks.

Common misuses and oversights sophisticated taxpayers still make

High-income taxpayers rarely make mistakes because they do not understand deductions. They make mistakes because the deduction is considered in isolation.

1. Treating asset acquisition as a year-end tax product

The weakest version of this strategy is simple: income is high, so the taxpayer buys something before year-end.

That may occasionally work, but it is not a planning framework. It ignores income character, deduction usability, liquidity, entity structure, and exit timing.

A serious acquisition plan starts before the income spike is finalized. It models the income, confirms whether the deduction can reach that income, decides how much liquidity should remain after closing, and shows what happens if the asset is sold earlier than expected.

2. Assuming cost segregation automatically reduces current tax

Cost segregation can be valuable, but it does not override passive activity rules, at-risk limits, basis limits, or poor investment economics.

Before commissioning a study, the taxpayer should understand whether the resulting deductions are expected to be currently usable, suspended for future use, or valuable only under a specific disposition strategy.

The study is a tool. The strategy is deciding whether accelerated depreciation improves the taxpayer’s multi-year position.

3. Ignoring placed-in-service timing

Buying an asset and placing it in service are not always the same event.

For depreciation purposes, the asset generally needs to be ready and available for its intended use. This matters for late-year acquisitions, renovations, short-term rentals, equipment purchases, and improvements that are not operational by year-end.

A taxpayer who waits until December to solve a tax problem may discover that the timing does not support the intended deduction. The calendar should be managed earlier.

4. Treating short-term rentals as automatic income offsets

Short-term rentals can create planning opportunities, but they also require classification and documentation discipline.

The taxpayer should analyze average rental periods, services provided, personal use, material participation, operating records, platform records, and whether the activity is being run consistently with the intended tax treatment.

A short-term rental strategy is not just a property acquisition. It is an operating model.

5. Forgetting NIIT in liquidity-event planning

High-income taxpayers often focus on capital gains and overlook NIIT.

The 3.8% NIIT can apply to certain net investment income above statutory thresholds, including capital gains and some rental income. In a liquidity-event year, NIIT should be modeled alongside ordinary income, capital gain, estimated tax payments, and reinvestment decisions.

For taxpayers already above the threshold, the question is not whether they are “high income.” The question is how much additional investment income is being added in the same year and whether any timing decisions can reduce tax compression.

6. Using the wrong entity for the long-term plan

Entity structure should be chosen for liability protection, financing, tax reporting, ownership transfers, estate planning, and exit flexibility.

An entity that seems adequate in the acquisition year can become inefficient when the taxpayer wants to refinance, admit investors, gift interests, exchange property, sell a partial interest, or reorganize before a liquidity event.

The structure should be tested against the most likely next transaction, not just the current purchase.

7. Failing to reserve for the tax cost of success

A good acquisition may appreciate. A business may grow. A rental property may produce taxable gain. A liquidity event may arrive earlier than expected.

The plan should assume success creates tax.

That means reserving for estimated taxes, depreciation-related gain, debt payoff, insurance shocks, repair costs, and reinvestment timing. A taxpayer who spends or reinvests all available liquidity may later be forced to sell, borrow, or disrupt a portfolio to pay tax.

What a coordinated acquisition plan should decide before capital is committed

A coordinated acquisition plan should produce decisions, not just observations.

| Planning Area | Decision to Make Before Acquisition |

|---|---|

| Income Calendar | Which years are expected to include ordinary income, capital gains, K-1 income, bonus income, lower-income gaps, or transaction proceeds? |

| Deduction Usability | Will depreciation, Section 179, operating losses, or investment-related deductions be currently usable, deferred, or suspended? |

| Activity Classification | Is the activity active, passive, rental, short-term rental, portfolio, or mixed, and what documentation supports that position? |

| Entity and Ownership Structure | Does the structure support liability protection, financing, tax reporting, investor admission, gifting, sale, exchange, and estate planning? |

| Financing | Does leverage improve after-tax return, or does it force a tax-motivated purchase with weak downside protection? |

| Liquidity Reserves | What cash must remain for taxes, insurance, repairs, vacancies, casualty exposure, debt service, and personal obligations? |

| Depreciation Profile | Should deductions be accelerated, smoothed, limited, or coordinated with expected future income? |

| Exit Options | Is the likely exit a taxable sale, refinance, §1031 exchange, installment sale, gift, estate hold, or business transition? |

| Advisor Coordination | Are the CPA, attorney, lender, financial advisor, and investment team working from the same multi-year model? |

This checklist is intentionally broader than a tax checklist. High-income taxpayers do not need isolated tactics. They need an acquisition model that shows what each tactic does to the next decision.

The most useful output is often a simple recommendation:

acquire now because the deduction is usable and the capital plan is durable

acquire now but finance differently to preserve liquidity

delay until the liquidity event closes and tax reserves are funded

buy in a different entity or ownership structure

use a smaller first acquisition and stage the rest

avoid the acquisition because the tax benefit is driving the decision

That kind of recommendation is more valuable than a large deduction with no strategy around it.

Review whether your entity, ownership, financing, and reserve plan still support the next transaction.

Commercial Real Estate Depreciation: What Actually Determines Whether It Works

A large depreciation deduction does not guarantee a current-year tax benefit. Whether real estate losses can offset W-2 or business income depends on passive activity rules, material participation, ownership structure, basis, and at-risk limits. The deduction has to reach the right income bucket before it produces any result — and confirming that is the first step, not an afterthought.

Cost segregation follows the same logic. It is most valuable when the deductions are usable in the near term, the hold period supports the strategy, and the exit plan accounts for future gain. If losses are likely to be suspended, a sale is approaching, or the study adds complexity without improving the multi-year position, the economics may not justify it. The building structure itself is generally not the primary target — the opportunity lies in shorter-lived components with recovery periods of 20 years or less, which may qualify for the 100% special depreciation allowance under current IRS guidance for qualifying property placed in service after January 19, 2025.

Once bonus depreciation is claimed, the decision is permanent. The opt-out election must be made by the return due date and cannot be reversed. Section 179 offers more flexibility — you can select the specific amount to expense each year, subject to the $2.56 million cap and taxable income limits — which is why it is often the better tool for the adjustable portion of a depreciation strategy. Bonus depreciation is most appropriate when full acceleration is certain to produce a benefit.

The permanent 100% bonus depreciation rate under the OBBBA removes the deadline pressure that defined planning under the TCJA phase-down, where rates were set to fall to 20% in 2026 and disappear by 2027. That sunset created artificial urgency. The permanent rate replaces urgency with discipline — the question is no longer whether you can beat a deadline, but when, given your lifetime tax curve, the deduction should be recognized.

Real Estate Professional Status and NIIT are commonly misread together. REPS reclassifies rental activities as non-passive, allowing losses to offset active income without limitation — but it does not remove rental income or capital gains from NIIT exposure. If MAGI exceeds the applicable threshold, net rental income generally remains subject to the 3.8% tax regardless of professional status. What reduces NIIT is reducing net investment income, and a well-timed cost segregation study can accomplish that directly. The greater risk is exit-year stacking — a real estate sale that lands in the same year as a business sale, bonus, Roth conversion, or trust distribution can produce a materially different result than the same transaction in a cleaner year.

Two points that often go unexamined: depreciation recapture only applies where a gain exists. A sale below adjusted basis produces a capital loss, not recapture income — though passive activity rules may limit the deductibility of that loss in the current year. And for investors who hold until death, the stepped-up basis permanently eliminates accumulated recapture, making front-loaded depreciation strategies asymmetrically favorable with no downstream cost.

Bring us the asset, income event, and likely exit timeline so we can evaluate the sequence before the purchase is finalized.

Conclusion

Aligning asset acquisition with income spikes, liquidity events, and business cycles is not about finding a deduction. It is about deciding when capital should be committed, how deductions should be used, where losses may be limited, and what the exit year will look like before the purchase is made.

For high-income Florida taxpayers, the strongest plans are federal-tax focused, real-estate aware, liquidity-conscious, and multi-year by design. They account for income character, activity classification, deduction usability, entity structure, NIIT, depreciation-related gain, Florida property economics, insurance exposure, and reserves.

The best acquisition decisions answer four questions clearly:

Why this asset? Why this year? Why this structure? What happens when we exit?

When those answers are coordinated, asset acquisition becomes part of a durable tax strategy rather than a reactive year-end move.

Asset Acquisition Tax Planning FAQs

Key questions for high-income taxpayers evaluating acquisition timing, liquidity events, passive losses, financing, Florida real estate reserves, and advisor coordination.

How should I decide whether to buy before or after a liquidity event?

We would start by separating the liquidity event from the acquisition decision. A sale year may already include capital gain, NIIT exposure, estimated tax obligations, legal fees, debt payoff, and reinvestment pressure. Buying before that stack is modeled can leave too little room for reserves or create deductions that do not offset the intended income. Buying after the event may provide cleaner liquidity and better pacing, but it can also miss a high-income planning window. The better answer comes from mapping closing dates, tax payment dates, reserve needs, and the first year the new asset can produce usable deductions.

What makes an asset acquisition tax-efficient beyond first-year depreciation?

A tax-efficient acquisition is one where the deduction, structure, financing, and exit plan work together. First-year depreciation can be valuable, but it is only one part of the model. We would also look at whether the deduction is usable, whether losses may be passive or limited, how much liquidity remains after closing, and whether the asset still makes sense if depreciation is less valuable than expected. A stronger acquisition plan also considers future income years, refinancing plans, potential sale timing, and whether the ownership structure preserves flexibility for the next transaction.

How do passive losses affect acquisition timing for high-income investors?

Passive losses can change the entire timing analysis because a deduction that looks valuable on paper may not reduce current tax. If the activity is passive, losses may be suspended until there is sufficient passive income or a qualifying disposition. That does not make the acquisition ineffective, but it changes how we measure value. Instead of treating the deduction as an immediate offset, we would model when the loss may become usable and whether that timing aligns with the investor’s income, cash flow, and exit plans. This is especially important for real estate acquisitions made during a high-income year.

When should financing be part of the tax planning discussion?

Financing should be discussed before the acquisition is made, not after the tax projection is prepared. Debt affects cash flow, reserves, basis, risk tolerance, and exit flexibility. A highly leveraged acquisition may improve return in one scenario but reduce liquidity if income falls, insurance costs rise, repairs accelerate, or the sale is delayed. We would also consider whether financing terms support the expected holding period and whether debt service competes with estimated tax payments or operating needs. Tax value should not be evaluated separately from capital structure.

How should Florida real estate investors think about reserves before acquiring another property?

For Florida real estate investors, reserves are part of the tax strategy because they determine whether the plan can survive the holding period. A property may produce depreciation benefits, but insurance, casualty exposure, repairs, vacancies, and debt service can absorb cash quickly. We would want reserves for taxes, insurance, capital expenditures, debt service, and unexpected property-level events before deciding how much capital should be committed. Under-reserving can force a sale, refinance, or portfolio disruption at the wrong time, which may undo the benefit of otherwise sound acquisition timing.

What should my CPA, attorney, lender, and advisor coordinate before I close?

Before closing, the advisor team should be working from the same multi-year model. The CPA should understand the expected income calendar, deduction usability, passive loss exposure, NIIT exposure, and depreciation profile. The attorney should confirm whether the entity and ownership structure support liability protection, financing, gifting, sale, or exchange planning. The lender should understand reserve needs and downside cash-flow assumptions. The investment advisor should account for liquidity, diversification, and reinvestment timing. The value is in coordination. A technically correct decision in one silo can still create friction in the next transaction.

When is delaying an acquisition the better tax strategy?

Delaying may be better when the tax benefit is driving the purchase more than the asset quality, or when the deduction is unlikely to be usable in the intended year. It may also make sense when a liquidity event has not closed, tax reserves are not funded, entity structure is unresolved, financing terms are weak, or the taxpayer expects a clearer income picture soon. Waiting is not the same as inaction. It can preserve optionality, improve documentation, protect liquidity, and allow the acquisition to be made in a structure that better supports the eventual exit.